Even though Medicare does come with deductibles, you can't contribute money to an HSA once you sign up for it. Therefore, if you have the option to hold off on enrolling in Medicare, it could pay to do so. Medicare and HSA contributions don't mix

Can an HRA pay Medicare premiums?

At first, reading the rules for employer payment of premiums under the Internal Revenue Service, Affordable Care Act, and Department of Labor, there seems to be no prohibition against employers having an HRA pay Medicare premiums the traditional GHP premium.

Are HRA contributions tax deductible?

As a benefit to employers, contributions to the HRA are 100% tax deductible. As an alternative to more expensive retiree healthcare, an employer may use HRA to cover the health costs of retired employees.

Who decides how much to contribute to an HRA?

The health reimbursement arrangement is funded solely by the employer, which also decides the maximum annual contribution for each employee’s HRA. Employers determine how much to contribute to employees’ HRAs, except that all workers in the same class of employees must receive the same contribution, as noted above.

Will my Individual Coverage HRA offer affect my marketplace benefits?

Your individual coverage HRA offer may impact employees’ and their dependents' eligibility for a premium tax credit that helps lower monthly insurance payments for Marketplace coverage.

What is HRA in Medicare?

Health reimbursement arrangements (HRAs) are a type of account-based health plan that employers can use to reimburse employees for their medical care expenses.

Can retirees have an HRA?

HRAs for retirees allow retired employees to use the funds allocated to their account to pay for health expenses during retirement, such as medical care, prescription drugs, and many health insurance premiums. Essentially, this product allows retirees to use their HRA dollars when and where they need it most.

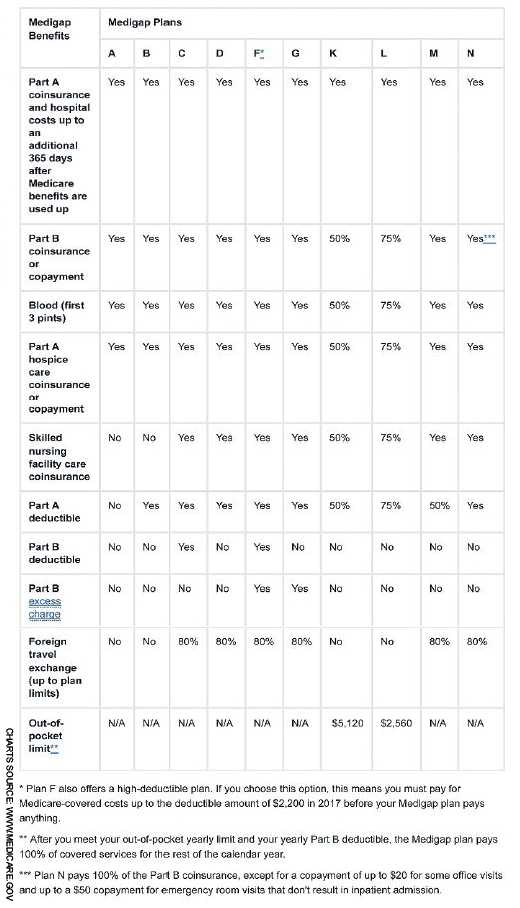

Can HRA be used to pay Medigap premiums?

Individual Coverage Health Reimbursement Arrangement (ICHRA) To be eligible for an Individual Coverage Health Reimbursement Arrangement, you'll need Medicare Part A and Part B, or Medicare Part C. You can use the ICHRA to reimburse premiums for Medicare and Medigap as well as other costs.

Can you add to an HRA?

The amount contributed to the HRA is up to the employer. For some HRAs, including the QSEHRA and the excepted benefit HRA, there are annual limits on contribution. For others, including the ICHRA, retiree HRA, and one-person stand-alone HRA, there are no contribution limits.

Can a retiree HRA reimburse Medicare premiums?

Can you reimburse their Medicare premiums through a retiree health reimbursement arrangement (HRA)? Answer: Yes. The IRS has provided that reimbursements for insurance covering medical care expenses, as defined in Internal Revenue Code Sec.

What is HRA retiree?

What is a Retiree HRA? A retiree health reimbursement arrangement (RHRA) is an employer-funded account designed to help retired employees pay for plan-eligible medical expenses during retirement, including individual health insurance and Medicare premiums.

Can you use HRA for dental?

You can use the funds in your HRA to pay for eligible medical expenses, as determined by the IRS and your employer. Some employers may only allow the HRA to pay for services covered by your health plan. Some employers may also let you use funds in the account to pay for dental, vision or other services.

What expenses qualify for HRA?

What could be an HRA eligible expense?Coinsurance and deductible expenses. These are both related to your insurance. ... Dental & vision care. If you have a Limited HRA, expenses related to these two categories will be the only ones eligible. ... Specialists or alternative medicine. ... Prescription drugs and OTC items.

What can I use my HRA to pay for?

HRAs can be used to pay for qualified medical expenses, which include prescription medications, insulin, an annual physical exam, crutches, birth control pills, meals paid for while receiving treatment at a medical facility, care from a psychologist or psychiatrist, substance abuse treatment, transportation costs ...

What is a disadvantage of a health reimbursement account?

No Portability One con for employees is that because HRAs are employer-funded, the employer owns the money in the account though it is there for the individual to use. If the person leaves the company or the job is terminated, the HRA money stays behind with the employer.

Who determines the eligibility and contribution limits in a HRA?

Your employer will determine the eligibility requirements for receiving HRA contributions. Generally, you must be enrolled in a specific health plan through the employer to receive the funds. Your employer may limit the expense types that can be reimbursed through the HRA.

Is an HRA worth it?

HRAs are an excellent way to provide a well-rounded health benefit and allow employees to pay for the specific medical expenses that meet their individual needs. It's an especially budget-friendly option for small businesses that can't afford a group health insurance plan.

Have more questions?

Here at Henderson Brothers, we want to provide you with the best and most accurate information available. You have the right to be correctly informed about your options, and we want to ensure that you are able to make the decisions that are best for you and your family. Please feel free to reach out to us if you have questions about your coverage or need assistance to find a new policy. We are licensed agents with expert knowledge who are ready to serve you. We look forward to hearing from you!

What is an HRA account?

Health Reimbursement Arrangement (HRA): The account allows you to be refunded by your employer for certain out-of-pocket healthcare expenses. HRAs often contain specific language about which claims are reimbursed and what you must provide to your employer for the reimbursement process. Some HRAs are designed to allow for a balance ...

How long does Medicare take to make Part A effective?

In many cases, Medicare will make Part A effective retroactively, up to six (6) months prior to your application date. Check with your local Social Security Office to find out when Part A would become effective for your particular situation.

Can HSA be used for QMEs?

In many ways like a 401 (k), the money deposited by an employer and/or an employee is most often a pre-tax payroll contribution. The HSA money can be invested in a guaranteed interested account or protected securities, and can be used to pay for any Qualified Medical Expenses (QMEs).

Is medical FSA pre-tax?

Medical Flexible Spending Account (FSA): Like the HSA, all money saved is pre-tax. Any money spent is also considered pre-tax. When the benefit year ends, any money not spent will be lost unless your employer’s plan contains a specific provision allowing for a small carry-over year after year.

What happens when an employer refuses to pay GHP?

When an employer allows an employee to refuse the employer-sponsored GHP so that the employer may then pay the employee’s Medicare premiums, the GHP disappears as primary payer. The result is shifting the burden of primary payer to Medicare in the absence of other coverage.

What is the MSP rule?

MSP rules determine which coverage pays first when a person is covered by both Medicare and a GHP. The goal is to strike a balance to protect both small-group employers and Medicare.

What is the age limit for Medicare?

Yet, the age to qualify for Medicare remains at 65 years old. This difference in eligibility age means more people are working while under Medicare coverage.

Is Medicare the primary payer for small groups?

This is not an issue with small groups because Medicare is always the primary payer for eligible employees in groups of fewer than 20 employees. For groups of 20+ employees, however, making Medicare the primary payer where it was not, has the potential to move a tremendous burden onto Medicare.

Can you leave GHP for Medicare?

That’s as long as employers do not encourage or force employees to leave the GHP for Medicare (so that the employer can save money with lower premiums). And there, the IRS refers employers to MSP rules.

Can an employer pay GHP premiums?

At first, reading the rules for employer payment of premiums under the Internal Revenue Service, Affordable Care Act, and Department of Labor, there seems to be no prohibition against employers having an HRA pay Medicare premiums the traditional GHP premium. That’s as long as employers do not encourage or force employees to leave ...

Can HRA pay Medicare premiums?

Can an HRA pay Medicare premiums for employees? For an employer-sponsored GHP with 20 or more employees, the answer is no. It is not permitted under Medicare Secondary Payer (MSP) rules.

Can I offer an individual coverage HRA?

Generally, employer s of any size can offer an individual coverage HRA, as long as they have one employee who isn’t a self-employed owner or the spouse of a self-employed owner. HRAs are only for employees, not self-employed individuals.

Will I qualify for the Small Business Health Care Tax Credit?

Enrolling in Small Business Health Options Program (SHOP) coverage is generally the only way to qualify for the Small Business Health Care Tax Credit, which can save you up to 50% of your employer contribution for 2 consecutive years. Learn more about offering traditional group coverage SHOP plans to your employees.

How much can I contribute to my employees’ costs?

There are no annual minimum or maximum contribution requirements.

How is “affordability” determined?

The Marketplace will determine if the offer meets requirements for “affordability,” which will help determine an employee’s eligibility for the premium tax credit. Prior to submitting a Marketplace application, employees can also use the HRA affordability tool for an estimate of their individual coverage HRA’s affordability.

What happens if an employee is not affordable?

If your offer is affordable: The employee won’t be eligible for the premium tax credit for the employee’s Marketplace coverage or the coverage of other household members who would be covered by the individual coverage HRA. If your offer isn’t affordable: The employee must decline (“opt out” of) the individual coverage HRA to claim ...

What is HRA in health insurance?

The individual coverage Health Reimbursement Arrangement (HRA) is an alternative to offering a traditional group health plan to your employees. It’s a specific account-based health plan that allows employers to provide defined non-taxed reimbursements to employees for qualified medical expenses, including monthly premiums and out-of-pocket costs, like copayments and deductibles. Employees must be enrolled in individual health insurance coverage (like a plan they bought through the Marketplace) to use the funds.

What does the Marketplace do?

The Marketplace will determine if the offer meets requirements for “affordability,” which will help determine an employee’s eligibility for premium tax credit. Prior to submitting a Marketplace application, employees can also use the HRA tool for an estimate of their individual coverage HRA’s affordability.

Who Funds an HRA?

HRAs are funded entirely by employer money. 4 An HRA is not an account (though you may see it mistakenly referred to that way). It’s a reimbursement arrangement between employee and employer. Employees can’t invest the balance, and it doesn’t earn interest. 2 If you participate in an HRA, you won’t see any deductions from your paycheck. 4

Can I Use an HRA and an FSA?

Yes, it is possible to have both an HRA and an FSA. 4 If you do, great—that’s even more untaxed income you can use for medical expenses. You can contribute up to $2,750 to an FSA in 2021 (rising to $2,850 in 2022), and your employer will take that money out of your paycheck. 12 3 11 However, do note that in most cases, you cannot use an HRA along with an HSA . 13

How are HRAs funded?

HRAs are funded entirely by employer money. 3 An HRA is not an account (though you may see it mistakenly referred to that way). It’s a reimbursement arrangement between employee and employer. Employees can’t invest the balance, and it doesn’t earn interest. 2 If you participate in an HRA, you won’t see any deductions from your paycheck. 3

When will HRAs start paying back?

Beginning in January 2020, employers of all sizes can offer to reimburse their employees for some of the cost of buying individual health insurance plans instead of offering group health insurance. These reimbursement arrangements, called individual coverage HRAs, can also pay employees back for qualified medical expenses such as coinsurance ...

What are qualified medical expenses?

Qualified medical expenses include costs like visiting the doctor when you’re sick, getting X-rays, or having surgery. Dental and vision expenses usually qualify, too, as do a few over-the-counter items, such as diabetes-testing aids, blood-pressure monitors, and contact-lens solution. 6.

Can an employee use an HRA?

In general, employees can use an HRA to be reimbursed for qualified medical expenses their health insurance doesn’t pay for, such as medical and pharmacy expenses they must pay out of pocket before meeting a deductible, as well as a coinsurance that applies after meeting a deductible. 3.

Can HRA verify a claim?

Your HRA administrator will often be able to verify your claim automatically, but sometimes you’ll need to submit an itemized bill from your healthcare provider to substantiate your claim. By law, no expense is too small to be reimbursed, but your employer might require you to accumulate a minimum amount of reimbursable expenses before it will issue a check.

What Is a Health Reimbursement Arrangement (HRA)?

A health reimbursement arrangement (HRA) is an employer-funded plan that reimburses employees for qualified medical expenses and , in some cases, insurance premiums. Employers are allowed to claim a tax deduction for the reimbursements they make through these plans, and reimbursement dollars received by employees are generally tax-free. 1 2

What is an HRA?

HRAs reimburse employees for certain medical expenses and sometimes insurance premiums. Employers, not employees, fund HRAs. An HRA is not portable; the employee loses this benefit when they leave the company. Government rules, which employers may refine further, determine which expenses can be reimbursed for employees.

What can HRAs be used for?

HRAs can be used to pay for qualified medical expenses, which include prescription medications, insulin, an annual physical exam, crutches, birth control pills, meals paid for while receiving treatment at a medical facility, care from a psychologist or psychiatrist, substance abuse treatment, transportation costs incurred to get medical care, and much more. Employees can also use HRAs to buy their own comprehensive individual health insurance with pretax dollars, through the aforementioned individual coverage HRA (ICHRA).

How much can a company reimburse employees in 2021?

The yearly limits are set by the Internal Revenue Service (IRS). For 2021, a company with a QSEHRA can reimburse individual employees for up to $5,300 per year and employees that have families for up to $10,700 per year. 3 The money that is reimbursed is tax-free for the employees and tax-deductible for the employers. 3

When will HRAs be available?

An Individual Coverage HRA (ICHRA) is relatively new, having only been available since January 2020. Previously, HRAs could not be used to pay for individual health insurance premiums. But as of January 2020, the government allows employers to offer their employees a new type of HRA called an individual coverage HRA—instead of group health insurance. 4

What expenses can be reimbursed by HRA?

Depending on the type of HRA, funds may be used to reimburse health insurance premiums, vision and dental insurance premiums, and qualified medical expenses.

What are the expenses not covered by a health reimbursement arrangement?

Maternity clothes, gym membership fees, marriage counseling, and childcare are among the expenses not covered by a health reimbursement arrangement (HRA).

What happens to HRA if you retire?

What happens to the money in my HRA if I leave my job or retire? The unused money stays with the company when an employee leaves their job, retires, or is let go . However, there is usually a 90-day runout period during when employees can submit reimbursement requests for expenses incurred during employment.

How does HRA work?

The HRA is 100 percent funded by the employer and the terms of these arrangements can provide first dollar medical coverage until the funds are exhausted or insurance coverage kicks in . The contribution amount per employee is set by the employer. The details can be a bit confusing, which is why we've compiled a list of most asked questions about HRA account rules.

What is an eligible health care expense for an HRA?

They include health insurance premiums, health insurance deductibles, coinsurance and copays, and other medical expenses. Eligible expenses must be incurred by the employee and their family and must take place within the HRA plan year.

What is HRA in health insurance?

A health reimbursement account (HRA), also known as a health reimbursement arrangement, is an IRS-approved, tax-advantaged, health benefit plan that reimburses employees for out-of-pocket medical expenses and individual health insurance premiums.

What can HRA money be used for?

HRA money can be used to pay for family medical expenses.

Does HRA earn interest?

Does the money in my HRA earn interest? Typically, no. Unless the HRA is being administered by a TPA, most HRA plan rules prohibit HRA funds from being held as individual owned bank account eligible for and able to earn interest. With platforms like PeopleKeep, the business keeps the funds until reimbursement requests are approved and the money is included on an employee's paycheck.

Is health care sharing ministry fee taxable?

Great question. Health care sharing ministry fees aren't considered eligible expenses for an HRA because these ministries don't provide health insurance. People belonging to a health care sharing ministry can still participate in some HRAs (like the QSEHRA), but they must do so on a taxable basis.

What is the maximum deductible for Medicare 2020?

For 2020, it means a deductible of at least $1,400 as an individual or $2,800 as a family. But what happens when you sign up for Medicare as your health insurance? ...

How long does it take to get Medicare?

Medicare eligibility begins at age 65, and your initial enrollment window spans seven months, starting three months before the month of your 65th birthday and ending three months after that month. If you don't sign up on time, you'll risk a 10% penalty on your Part B premiums for life (Part A doesn't typically charge a premium to begin with, so there's no financial hit there if you sign up late).

What is the difference between an FSA and an HSA?

With an FSA, you must deplete your plan balance year after year , or you risk losing your remaining funds. An HSA , on the other hand, lets you contribute funds that never expire. In fact, the purpose of an HSA is to put in more money than you need in the near term, and then invest your balance for added growth. ...

Is HSA tax free?

IMAGE SOURCE: GETTY IMAGES. The beauty of the HSA is that it's triple tax-advantaged. Contributions are made on a pre-tax basis, investments gains aren't taxed, and withdrawals are tax-free provided they're used for qualified medical expenses. There is, however, one major catch when it comes to HSAs, and it's that not everyone can qualify ...

Can seniors sign up for Medicare?

Many seniors jump to sign up for Medicare as soon as they're able, but if doing so prevents you from contributing to an HSA, then you may want to consider delaying enrollment. This especially holds true if you get good coverage from your group health plan and are able to manage your existing deductibles under it.

Who is Maurie Backman?

Maurie Backman is a personal finance writer who's passionate about educating others. Her goal is to make financial topics interesting (because they often aren't) and she believes that a healthy dose of sarcasm never hurt anyone. In her somewhat limited spare time, she enjoys playing in nature, watching hockey, and curling up with a good book.

Does Motley Fool have a disclosure policy?

The Motley Fool has a disclosure policy.

What is HRA reimbursement?

It depends on which HRA you choose! Health reimbursement arrangements are tax-advantaged benefits solutions built on a series of regulations that help to ensure they are being offered fairly and are achieving their intended aim, which is to help employees pay for benefits tax-free.

Can you contribute to a QSEHRA?

Just to be clear though—employees cannot contribute to a QSEHRA (they would just pay out of their own pocket) As we’ve already seen, while there aren’t any contribution limits with ICHRA, there is the issue of how little you can actually contribute, which changes from year to year.

Can you take QSEHRA in January?

All QSEHRA reimbursements are subject to annual maximums and become available to employees on a monthly basis. This means employees can’t take the full annual amount in January—instead, the funds become available to employees each month.