| Medicare plan | Typical monthly cost |

|---|---|

| Part B (medical) | $170.10 |

| Part C (bundle) | $33 |

| Part D (prescriptions) | $42 |

| Medicare Supplement | $163 |

How much does Medicare Part a cost?

Medicare costs at a glance. Most people don't pay a monthly premium for Part A (sometimes called " premium-free Part A "). If you buy Part A, you'll pay up to $437 each month. If you paid Medicare taxes for less than 30 quarters, the standard Part A premium is $437. If you paid Medicare taxes for 30-39 quarters, the standard Part A premium is $240.

How much does Medicare Advantage cost a month?

In 2021, seniors paid an average of $21 a month for their Medicare Advantage plans. Available plans vary by state, and monthly premiums vary too: Some plans pay for a person’s Medicare Part B premiums, while other plans include extra benefits, like dental and vision coverage.

How much does Medicare supplement insurance cost per month?

Wisconsin, Hawaii and Iowa had the plans with the lowest average monthly premiums, around $102 per month. The highest average monthly Medigap premiums were in New York, at $304.72 per month. Learn more about Medicare Supplement Insurance plans in your state. How much do Medicare Part A and Part B cost in 2021?

How much does it cost to work with a Medicaid planner?

The average cost of working with a Medicaid planning professional is generally less than the cost of one month’s care in a nursing home. There are a wide variety of costs associated with engaging a Medicaid Planner. This depends on the type of Planner as well as the needs of the applicant.

How much do Medicare supplement plans usually cost?

In 2020, the average premium for Medicare supplemental insurance, or Medigap, was approximately $150 per month or $1,800 per year, according to Senior Market Sales, a full-service insurance organization.

How Much Does Medicare pay for a routine office visit?

Everyone with Medicare is entitled to a yearly wellness visit that has no charge and is not subject to a deductible. Beyond that, Medicare Part B covers 80% of the Medicare-approved cost of medically necessary doctor visits. The individual must pay 20% to the doctor or service provider as coinsurance.

What are the negatives of a Medicare Advantage plan?

Medicare Advantage can become expensive if you're sick, due to uncovered copays. Additionally, a plan may offer only a limited network of doctors, which can interfere with a patient's choice. It's not easy to change to another plan. If you decide to switch to a Medigap policy, there often are lifetime penalties.

What is the difference between Medicare and Medicare Advantage plans?

Medicare Advantage is an “all in one” alternative to Original Medicare. These “bundled” plans include Part A, Part B, and usually Part D. Plans may have lower out-of- pocket costs than Original Medicare. In many cases, you'll need to use doctors who are in the plan's network.

How often can you have a Medicare Annual Wellness visit?

once every 12 monthsHow often will Medicare pay for an Annual Wellness Visit? Medicare will pay for an Annual Wellness Visit once every 12 months.

Does Medicare cover an annual wellness visit?

If you qualify, Original Medicare covers the Annual Wellness Visit at 100% of the Medicare-approved amount when you receive the service from a participating provider. This means you pay nothing (no deductible or coinsurance).

What are the top 3 Medicare Advantage plans?

The Best Medicare Advantage Provider by State Local plans can be high-quality and reasonably priced. Blue Cross Blue Shield, Humana and United Healthcare earn the highest rankings among the national carriers in many states.

Why do I need Medicare Part C?

Medicare Part C provides more coverage for everyday healthcare including prescription drug coverage with some plans when combined with Part D. A Medicare Advantage prescription drug (MAPD) plan is when a Part C and Part D plan are combined. Medicare Part D only covers prescription drugs.

Why are Medicare Advantage plans being pushed so hard?

Advantage plans are heavily advertised because of how they are funded. These plans' premiums are low or nonexistent because Medicare pays the carrier whenever someone enrolls. It benefits insurance companies to encourage enrollment in Advantage plans because of the money they receive from Medicare.

What is the most popular Medicare Advantage plan?

AARP/UnitedHealthcare is the most popular Medicare Advantage provider with many enrollees valuing its combination of good ratings, affordable premiums and add-on benefits. For many people, AARP/UnitedHealthcare Medicare Advantage plans fall into the sweet spot for having good benefits at an affordable price.

Is Medicare Advantage more expensive than Medicare?

Slightly more than half of all Medicare Advantage enrollees would incur higher costs than beneficiaries in traditional Medicare with no supplemental coverage for a 6-day hospital stay, though cost are generally lower in Medicare Advantage for shorter stays.

Is Original Medicare more expensive than Medicare Advantage?

The costs of providing benefits to enrollees in private Medicare Advantage (MA) plans are slightly less, on average, than what traditional Medicare spends per beneficiary in the same county.

What is the cost of a wellness visit?

The cost of a basic wellness exam ranged from $75 to over $300. Below is the average cost of a basic primary care visit without any additional lab testing, immunizations, or other services.

Does Medicare Part B cover 100 percent?

Generally speaking, Medicare reimbursement under Part B is 80% of allowable charges for a covered service after you meet your Part B deductible. Unlike Part A, you pay your Part B deductible just once each calendar year. After that, you generally pay 20% of the Medicare-approved amount for your care.

Does Medicare Part B cover doctor visits?

Medicare Part B pays for outpatient medical care, such as doctor visits, some home health services, some laboratory tests, some medications, and some medical equipment. (Hospital and skilled nursing facility stays are covered under Medicare Part A, as are some home health services.)

What percentage does Medicare cover?

Medicare Part B pays 80% of the cost for most outpatient care and services, and you pay 20%. For 2022, the standard monthly Part B premium is $170.10.

Medicare Advantage Plan (Part C)

Monthly premiums vary based on which plan you join. The amount can change each year.

Medicare Supplement Insurance (Medigap)

Monthly premiums vary based on which policy you buy, where you live, and other factors. The amount can change each year.

What is the second most popular Medicare plan?

Medigap Plan G is, in fact, the second-most popular Medigap plan. 17 percent of all Medigap beneficiaries are enrolled in Plan G. 2. The chart below shows the average monthly premium for Medicare Supplement Insurance Plan G for each state in 2018. 3.

How to contact Medicare Advantage 2021?

New to Medicare? Compare Medicare plan costs in your area. Compare Plans. Or call. 1-800-557-6059. 1-800-557-6059 TTY Users: 711 to speak with a licensed insurance agent.

Which states have the lowest Medicare premiums?

Florida, South Carolina, Nevada, Georgia and Arizona had the lowest weighted average monthly premiums, with all five states having weighted average plan premiums of $17 or less per month. The highest average monthly premiums were for Medicare Advantage plans in Massachusetts, North Dakota and South Dakota. *Medicare Advantage plans are not sold in ...

How much does Medicare pay for seniors?

In 2019, seniors paid an average of $29 a month for their Medicare Advantage plans. Available plans vary by state, and monthly premiums vary too: Some plans pay for a person’s Medicare Part B premiums, while other plans include extra benefits, like dental and vision coverage.

What is the cheapest Medicare plan for seniors?

With an average $23 monthly premium, HMO plans were the cheapest option for seniors in 2019.

Why do seniors not have to pay Medicare Part D?

Many plans eliminate the need for Medicare Part D because they include prescription drug coverage. Seniors pay a premium for their Medicare Advantage Plans every month. They also pay a deductible on covered services, and coinsurance after they’ve met the deductible.

Why do people choose Medicare Advantage?

Many individuals beyond retirement age opt for Medicare Advantage Plans because they reduce annual out-of-pocket health care costs. They feel familiar, too, because they’re essentially the same as other health insurance plans.

Can I get Medicare Part A for free?

Most retirees qualify for premium-free Medicare Part A. Seniors who paid Medicare taxes for less than 40 quarters aren’t automatically eligible to receive free Medicare Part A, but they can buy into the plan by paying a monthly fee.

Do seniors need to sign up for Medicare Part B?

Seniors don’t need to buy Medicare Part B if they decide to opt for Original Medicare; however if they want a Medicare Advantage Plan, they usually do need to sign up for Medicare Part B. Again, some Medicare Advantage Plans pay Medicare Part B costs to the government on a policyholder’s behalf.

What is the average Medicare Part D premium for 2021?

The average Part D plan premium in 2021 is $41.64 per month. 1. Because Original Medicare (Part A and Part B) does not cover retail prescription drugs in most cases, millions of Medicare beneficiaries turn to Medicare Part D or Medicare Advantage prescription drug (MA-PD) plans to get help paying for their drugs.

How much is Medicare Part D 2021?

How much does Medicare Part D cost? As mentioned above, the average premium for Medicare Part D plans in 2021 is $41.64 per month. The table below shows the average premiums and deductibles for Medicare Part D plans in 2021 for each state. Learn more about Medicare Part D plans in your state.

What is the Medicare donut hole?

After 2020, Medicare Part D plans have a shrunken coverage gap, or “donut hole,” which represents a temporary limit on what the plan will cover for prescription drugs. You enter the Part D donut hole once you and your plan have spent a combined $4,130 on covered drugs in 2021.

What is coinsurance and copayment?

Copayments and coinsurance are the amounts that you must pay once your plan’s coverage does begin. A copayment is usually a fixed dollar amount (such as $5) while coinsurance is most often a percentage of the cost (such as 20 percent). Plans might have different copayment or coinsurance amounts for each tier of drugs.

What is Part D premium?

Your Part D deductible is the amount that you must spend out of your own pocket for covered drugs in a calendar year before the plan kicks in and begins providing coverage.

How much will Part D cost in 2021?

You enter the Part D donut hole once you and your plan have spent a combined $4,130 on covered drugs in 2021. Once you reach the coverage gap, you will pay up to 25 percent of the cost of covered brand name and generic drugs until you reach total out-of-pocket spending of $6,550 for the year in 2021.

Who sells Medicare Part D?

Medicare Part D plans are sold by private insurance companies . These insurance companies are generally free to set their own premiums for the plans they sell. Medicare Part D plan costs in any particular area may depend partly on the cost of other plans being sold in the same area by competing carriers. Cost-sharing.

How much does Medicare cost in 2021?

There’s no simple answer to this question. Medicare Supplement plans can range from $50-$300+ in monthly premiums.

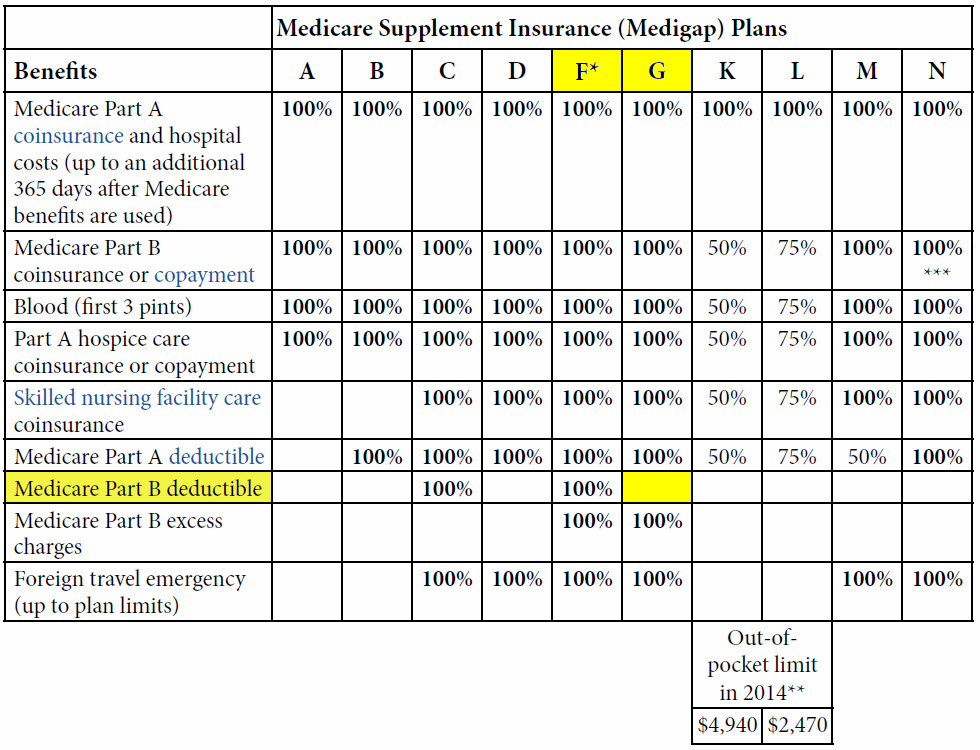

What is the letter plan on Medigap?

The letter plan itself is a factor that affects your Medigap premium rates. Less popular Medigap plans are priced differently than the top three. This is due to the lesser benefits they offer. Let’s take a look at sample rates for the rest of the Medigap plans, using Florida as the location.

What is Plan N?

Plan N is another popular Medigap plan option. Except for Part B excess charges, it covers everything Plan G covers. This is not a downside if you live in a state that doesn’t allow excess charges to begin with. Plan N Average Monthly Cost in Palm Harbor, FL (34684)*.

Is Plan F deductible?

There’s also a high-deductible version of Plan F. High-Deductible Plan F offers the same benefits as standard Plan F. Premiums for this plan are lower, but there’s a higher deductible the beneficiary must reach before the plan covers all costs.

Is Plan G the same as Plan F?

A high-deductible version of Plan G is also available. It offers the same benefits as standard Plan G. High-Deductible Plan G requires a higher deductible in exchange for lower monthly premiums, like Plan F’s high-deductible option before it.

Is New York a Medigap state?

You might have noticed that New York is not one of those states. You’ll also see it’s best to enroll in a Medigap plan when you become eligible at 65 instead of waiting. Premiums are always subject to increase every year, but you will likely start with higher premiums the older you are when you enroll.

What is Medicaid planner?

Medicaid Planners help clients structure their financial resources and prepare documentation to ensure the best possibility of being accepted into the Medicaid program. They create trusts, manage asset transfers, and convert countable assets into exempt assets to ensure eligibility and preserve a family’s resources.

How long does it take to get a medicaid plan?

Putting the plan into action can take longer. Depending on the strategy, it can take several weeks or months, even up to 6 months in some cases. In situations where there is an immediate need for Medicaid care, the Medicaid application documentation can be prepared concurrent with the execution of the plan.

How long does it take for a mistake to affect Medicaid eligibility?

It is worth noting that a mistake in planning can impact eligibility for as long as 5 years (2.5 years in California). This is because Medicaid has a look-back period. If one is not confident in their family’s ability to manage some complex legal and financial techniques, using a planner is advised.

What is a life resource planner?

A category of professionals called Life Resource Planners, or sometimes Eldercare Resource Planners, offer an alternative to traditional Medicaid planning. These advisors take a larger, holistic view of how to help families plan for paying for aging care. While Medicaid Planners are very focused on the task of helping families qualify for Medicaid, Life Resource Planners also look to see what other options exist and are available. As with Medicaid Planning professionals, their fees must be paid for out-of-pocket. However, those fees are substantially lower. Eldercare Resource Planners typically charge 50% – 75% less than Medicaid Planners. Learn more.

Do life resource planners have to pay for out of pocket?

As with Medicaid Planning professionals, their fees must be paid for out-of-pocket. However, those fees are substantially lower.

Is it necessary to retain a Medicaid planning professional?

For those who don’t qualify for free assistance, it is not absolutely necessary that they retain the services of a Medicaid Planning professional. However, in many situations it is prudent, cost-effective, and strongly advised. The decision should be based on each family’s specific situation.

Is it necessary to hire a medicaid planner?

Many families wonder if it is really necessary to hire a Medica id planner. There are two ways to answer this question. First, there are public employees that offer free assistance, so hiring a Medicaid Planner is not always necessary. However, not everyone is qualified to receive free assistance.

What is a commission based Medicaid planner?

This category of Medicaid planners, commission-based, is focused on helping individuals whose assets exceed Medicaid eligibility limits. They provide free services to families and individuals and take a commission when they purchase Medicaid compliant annuities to help applicants meet the Medicaid asset limits. While typically very knowledgeable about Medicaid eligibility, they are less familiar with alternatives to Medicaid, and do not have an incentive to advise clients in those areas. Since they are only compensated through the purchase of annuities, they are unlikely to assist individuals who are not in the position to purchase one. Commission-based Medicaid planners tend to advertise their services under Asset Protection. One should proceed with caution when working with an annuity salesperson / commission-based Medicaid planner.

How much does a Medicaid attorney cost?

On the downside, hiring an attorney is, far and away, the most expensive Medicaid planning option. Depending on the state, fees can range from $300 – $600 per hour.

What is a public benefits counselor?

Public benefits counselors / case managers work for state agencies at Area Agencies on Aging (AAAs), Aging and Disability Resource Centers (ADRCs), or Medicaid offices. They have a good understanding of Medicaid eligibility, as well as the alternatives to Medicaid. Also, on the positive side, they do not charge for their services.

What is the benefit of a care manager?

One major benefit is that typically care managers are very knowledgeable about local programs that provide assistance as alternatives to Medicaid. Since their primary expertise is care management, and hence, a client-centered approach, they are well aware of the individual’s care needs.

What is a health insurance counselor?

State Health Insurance Programs Counselors, often called SHIPs Counselors, are individuals who are usually volunteers, trained by the state to be knowledgeable about the existence of public benefits, such as Medicare and Medicaid.

Is it good to work with an eldercare financial planner?

The major positive aspect of working with an eldercare financial planner is that they have a very broad understanding of all the financial options available to seniors. Financial planners are a good option when there exists a variety of options for funding, such as life insurance settlements and reverse mortgages.

Is Medicaid a federal program?

In addition, Medicaid planning can be difficult because while Medicaid is a Federal program, it is administered on a state level, and the regulations and rules (such as eligibility) that govern it can vary greatly by state. Even within a state, Medicaid laws and programs may regularly change.

What is a CMP in Medicaid?

A CMP is a professional in the Medicaid field who is certified by the Certified Medicaid Planning Governing Board. Certification is received after a final certification exam is passed.

What is a CMP for a funeral home?

Funeral home directors. A CMP’s goal is to give you the most cost-effective and legal plan that’s the best fit for your Medicaid situation. Not everyone’s Medicaid path is the same. A CMP should help you navigate your specific Medicaid strategy as well as implementing that strategy.

Is Medicaid one size fits all?

Medicaid isn’t one-size-fits-all, and what someone else qualifies formight not be the best fit for you. After you and your CMP have developed your tailor-made Medicaid plan, they can even submit your application on your behalf or help you with any Medicaid-related issues going forward.

Can you go through the maze of medicaid alone?

Going through the maze of Medicaid isn’t the easiest task, and you shouldn’t feel obligated to navigate it alone. Finding a Certified Medicaid Planner gives you the chance not only to learn what you’re eligible for, but it’s someone who can tailor-make a plan that’s best for you.

Is Medicaid a federal program?

Medicaid isn’t the easiest federal program to navigate. A Certified Medicaid Planner (CMP) can help. A CMP has expert-level experience with Medicaid program and can help people navigate both current and new Medicaid rules. If you need help navigating Medicare, learn what it is and why one might be a good fit for you.