Can you get Medicare if you are still working?

Feb 08, 2022 · When to Sign Up for Medicare When Still Working You can (and should) enroll in Part A as soon as you’re eligible, regardless of your working status. If your company has fewer than 20 employees, you’ll likely need to enroll in Part B. Those enrolled in Part A who want prescription drug coverage – but ...

Does Medicare coverage change if you return to work?

Generally, if you have job-based health insurance through your (or your spouse’s) current job, you don’t have to sign up for Medicare while you (or your spouse) are still working. You can wait to sign up until you (or your spouse) stop working or you …

Will I be automatically enrolled in Medicare at 65?

Medicare eligibility starts at age 65. Your initial window to enroll is the seven-month period that begins three months before the month of your 65th birthday and ends three months after it. Seniors are generally advised to sign up on time to avoid penalties that could prove quite costly over the course of retirement.

When should I sign up for Medicare?

Mar 18, 2022 · As a financial advisor helping clients with their Medicare decisions, I’m frequently asked if they need to enroll in Medicare while working. When I …

When should I start my Medicare application?

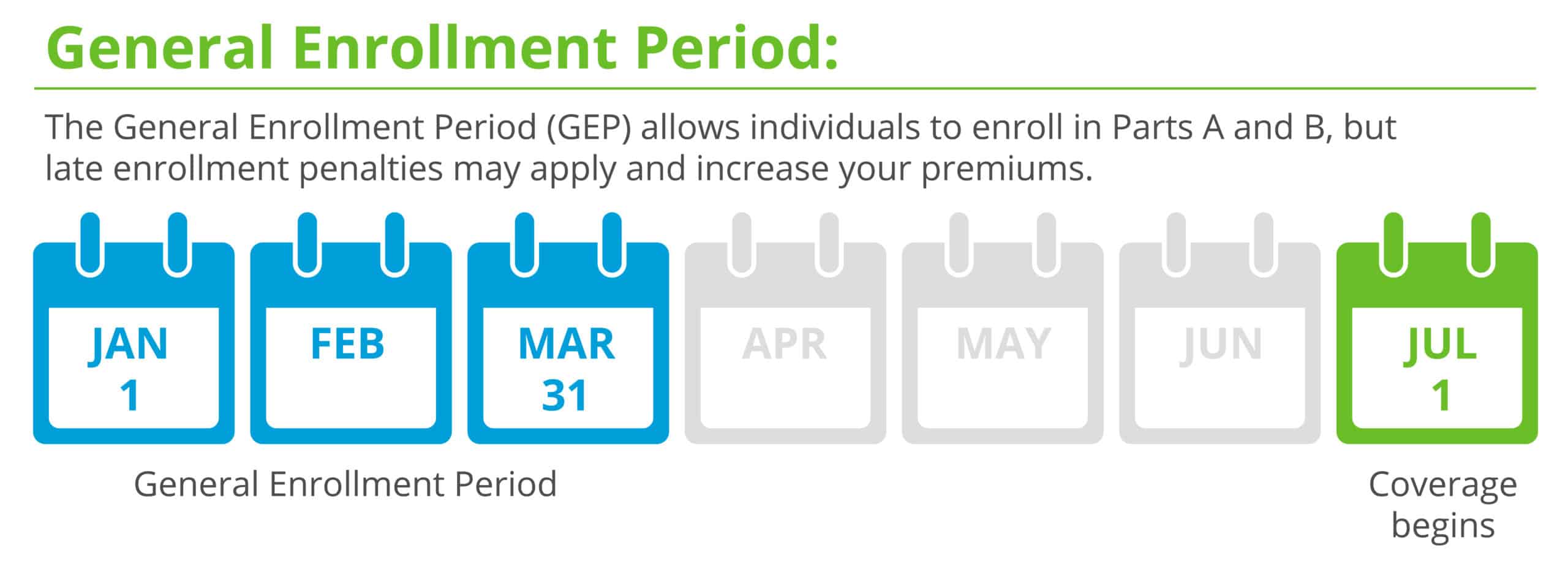

Generally, you're first eligible starting 3 months before you turn 65 and ending 3 months after the month you turn 65. If you don't sign up for Part B when you're first eligible, you might have to wait to sign up and go months without coverage.

Can I switch to Medicare while still working?

Generally, if you have job-based health insurance through your (or your spouse's) current job, you don't have to sign up for Medicare while you (or your spouse) are still working. You can wait to sign up until you (or your spouse) stop working or you lose your health insurance (whichever comes first).

What happens if you don't enroll in Medicare Part A at 65?

If you don't have to pay a Part A premium, you generally don't have to pay a Part A late enrollment penalty. The Part A penalty is 10% added to your monthly premium. You generally pay this extra amount for twice the number of years that you were eligible for Part A but not enrolled.

What happens if you don't enroll in Medicare in time?

Specifically, if you fail to sign up for Medicare on time, you'll risk a 10 percent surcharge on your Medicare Part B premiums for each year-long period you go without coverage upon being eligible. (Since Medicare Part A is usually free, a late enrollment penalty doesn't apply for most people.)

Can you have a HSA with Medicare?

Yes. Medicare doesn't offer an HSA qualifying option. You can't make contributions to your HSA for any months after you enroll in any part of Medicare, even if you're also covered on an HSA qualifying plan.

Are you automatically enrolled in Medicare if you are on Social Security?

Yes. If you are receiving benefits, the Social Security Administration will automatically sign you up at age 65 for parts A and B of Medicare. (Medicare is operated by the federal Centers for Medicare & Medicaid Services, but Social Security handles enrollment.)

Does Medicare coverage start the month you turn 65?

For most people, Medicare coverage starts the first day of the month you turn 65. Some people delay enrollment and remain on an employer plan. Others may take premium-free Part A and delay Part B. If someone is on Social Security Disability for 24 months, they qualify for Medicare.

What is the penalty for canceling Medicare Part B?

Your Part B premium penalty is 20% of the standard premium, and you'll have to pay this penalty for as long as you have Part B. (Even though you weren't covered a total of 27 months, this included only 2 full 12-month periods.) Find out what Part B covers.

Can I get Medicare Part B for free?

While Medicare Part A – which covers hospital care – is free for most enrollees, Part B – which covers doctor visits, diagnostics, and preventive care – charges participants a premium. Those premiums are a burden for many seniors, but here's how you can pay less for them.Jan 3, 2022

What is the grace period for Medicare payment?

When you're in traditional Medicare The original billing notice is the regular one that requests payment by a specified due date — the 25th of the month. The grace period for paying this bill is three months, ending on the last day of the third month after the month in which the bill was sent.Mar 26, 2016

What will Irmaa be in 2021?

C. IRMAA tables of Medicare Part B premium year for three previous yearsIRMAA Table2021More than $111,000 but less than or equal to $138,000$297.00More than $138,000 but less than or equal to $165,000$386.10More than $165,000 but less than $500,000$475.20More than $500,000$504.9012 more rows•Dec 6, 2021

What are the income limits for Medicare 2021?

In 2021, the adjustments will kick in for individuals with modified adjusted gross income above $88,000; for married couples who file a joint tax return, that amount is $176,000. For Part D prescription drug coverage, the additional amounts range from $12.30 to $77.10 with the same income thresholds applied.Nov 10, 2020

How long does it take to get Medicare?

Learn how to make sure they have health insurance once you’re enrolled. Medicare eligibility starts at age 65. Your initial window to enroll is the seven-month period that begins three months before the month of your 65th birthday and ends three months after it. Seniors are generally advised to sign up on time to avoid penalties ...

What happens if you don't sign up for Medicare?

Specifically, if you fail to sign up for Medicare on time, you’ll risk a 10 percent surcharge on your Medicare Part B premiums for each year-long period you go without coverage upon being eligible.

Does Medicare pay for Part A?

That said, it often pays to enroll in Medicare Part A on time even if you have health coverage already. It won’t cost you anything, and this way, Medicare can serve as your secondary insurance and potentially pick up the tab for anything your primary insurance (in this case, your work health plan) doesn’t cover.

You will be retired when you are 65

First, let’s go over the easiest scenario. If you are not working when you turn 65, and you are not covered by your spouse’s work coverage, then signing up for Medicare is an easy decision. If you are already talking Social Security, you should automatically be enrolled in Part A and Part B.

You are still working when you turn 65

While Medicare is designed to start the month you turn 65, there are exceptions, especially if you are still working and have creditable coverage, which most work coverage is. If you have creditable coverage, you can postpone Medicare without any penalties. This allows you to not pay for Medicare while also paying for work coverage.

Your spouse is still working when you turn 65

If your spouse still has work coverage when you turn 65, you have a few options. The first is just to stay on your spouse’s work coverage and delay taking full Medicare. In this case, you would follow the same instructions we gave above for people who are still working when they turn 65.

What happens if you don't sign up for Medicare?

Therefore, if you fail to sign up for Medicare when required, you will essentially be left with no coverage. It’s therefore extremely important to ask the employer whether you are required to sign up for Medicare when you turn 65 or receive Medicare on the basis of disability.

How long can you delay Medicare?

As long as you have group health insurance from an employer for which you or your spouse actively works after you turn 65, you can delay enrolling in Medicare until the employment ends or the coverage stops (whichever happens first), without incurring any late penalties if you enroll later. When the employer-tied coverage ends, you’re entitled to a special enrollment period of up to eight months to sign up for Medicare.

Can you sell a Medigap policy?

Insurance companies are prohibited from refusing to sell you a Medigap policy or charge higher premiums based on your health or preexisting medical conditions, if you buy the policy within six months of enrolling in Part B. Outside of that six-month window, except in very limited circumstances, they can do both.

Can you delay Medicare enrollment?

You can’t delay Medicare enrollment without penalty if your employer-sponsored coverage comes from retiree benefits or COBRA — by definition, these do not count as active employment. Nor does it count if you work beyond 65 but rely on retiree benefits from a former employer.