Where do I report my insurance premiums on my 1099-R?

Feb 03, 2020 · medicare premiums not shown on 1099 r. Medicare premium payments would not show up in a 1099 R but generally show up in a 1099 SSA social security tax statement. These are claimed as an itemized medical expenses as medical premiums only if you can claim itemized expenses during the year.

Can I deduct my insurance premiums on my 1099-R?

Feb 06, 2019 · The RRB only shows the total Part B, C, and/or D Medicare premiums that were deducted from railroad retirement annuity payments for the tax year indicated on Form RRB-1099-R. The RRB does not show the Medicare premiums deducted from social security benefits on any tax statement issued by the RRB. In addition, Medicare premium refunds are not included in …

Where can I find more information about 1099-R pension and Annuity Income?

For section 1035 exchanges that are reportable on Form 1099-R, enter the total value of the contract in box 1, 0 (zero) in box 2a, the total premiums paid in box 5, and Code 6 in box 7. Designated Roth account distributions.

What is the tax code for a 1099-R?

6050Y must be reported on Form 1099-R. Reportable disability payments made from a retirement plan must be reported on Form 1099-R. Generally, do not report payments subject to withholding of social security and Medicare taxes on this form. Report such payments on Form W-2, Wage and Tax Statement. Generally, do not report amounts totally exempt from

Where do you report health insurance premiums on 1099-R?

Where are Medicare premiums reported?

Are Medicare premiums included in taxable income?

What is Box 7 on a 1099-R?

Are Medicare premiums tax-deductible IRS?

Are Medicare premiums tax-deductible for retirees?

Can I deduct Medicare supplemental insurance premiums?

Are Medicare premiums deductible in 2020?

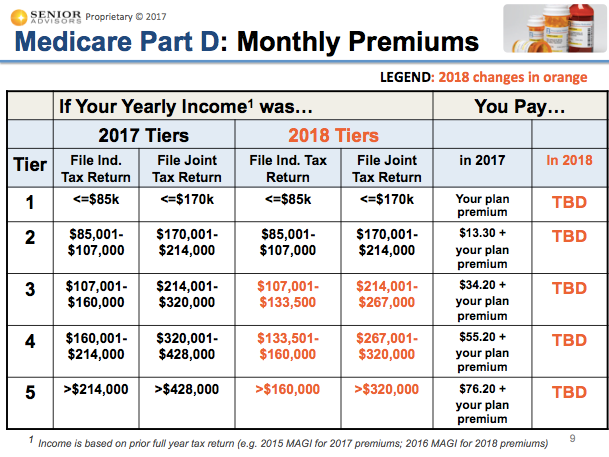

What income is used to determine Medicare premiums?

What does 7D mean on a 1099-R?

What does Box 5 Mean on a 1099-R?

What is Box 2a on 1099-R?

What is a 1099-R?

File Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans , IRAs, Insurance Contracts, etc., for each person to whom you have made a designated distribution or are treated as having made a distribution of $10 or more from profit-sharing or retirement plans, any individual retirement arrangements (IRAs), annuities, pensions, insurance contracts, survivor income benefit plans, permanent and total disability payments under life insurance contracts, charitable gift annuities, etc.

Who must file 1099-R?

The payer, trustee, or plan administrator must file Form 1099-R using the same name and employer identification number (EIN) used to deposit any tax withheld and to file Form 945, Annual Return of Withheld Federal#N#Income Tax.

What is the 2020-62 notice?

Notice 2020-62 contains the two model notices that may be provided to recipients of eligible rollover distributions to satisfy the notice requirements under section 402 (f). See Explanation to Recipients Before Eligible Rollover Distributions (Section 402 (f) Notice), later.

What is a direct rollover distribution?

A direct rollover is the direct payment of the distribution from a qualified plan, a section 403 (b) plan, or a governmental section 457 (b) plan to a traditional IRA, Roth IRA, or other eligible retirement plan. For additional rules regarding the treatment of direct rollovers from designated Roth accounts, see Designated Roth accounts, later. A direct rollover may be made for the employee, for the employee's surviving spouse, for the spouse or former spouse who is an alternate payee under a qualified domestic relations order (QDRO) or for a nonspouse designated beneficiary, in which case the direct rollover can only be made to an inherited IRA. If the distribution is paid to the surviving spouse, the distribution is treated in the same manner as if the spouse were the employee. See Part V of Notice 2007-7, 2007-5 I.R.B. 395, available at IRS.gov/irb/2007-05_IRB#NOT-2007-7, which has been modified by Notice 2009-82, 2009-41 I.R.B. 491, available at IRS.gov/irb/2009-41_IRB#NOT-2009-82, and Notice 2020-51, 2020-29 I.R.B. 73, available at IRS.gov/irb/2020-29_IRB#NOT-2020-51, for guidance on direct rollovers by nonspouse designated beneficiaries. Also, see Notice 2008-30, Part II, 2008-12 I.R.B. 638, available at IRS.gov/irb/2008-12_IRB#NOT-2008-30, which has been amplified and clarified by Notice 2009-75, 2009-39 I.R.B. 436, available at IRS.gov/irb/2009-39_IRB#NOT-2009-75, for questions and answers covering rollover contributions to Roth IRAs.

How long to provide 403b notice?

The explanation must be provided no more than 180 days and no fewer than 30 days before making an eligible rollover distribution or before the annuity starting date. However, if the recipient who has received the section 402 (f) notice affirmatively elects a distribution, you will not fail to satisfy the timing requirements merely because you make the distribution fewer than 30 days after you provided the notice as long as you meet the requirements of Regulations section 1.402 (f)-1, Q/A-2. The electronic section 402 (f) notice must meet the requirements for using electronic media in Regulations section 1.401 (a)-21.

Do you report a transfer from one IRA to another?

Generally, do not report a transfer between trustees or issuers that involves no payment or distribution of funds to the participant, including a trustee-to-trustee transfer from one IRA to another IRA, valid transfers from one section 403 (b) plan in accordance with paragraphs 1 through 3 of Regulations section 1.403 (b)-10 (b), or for the purchase of permissive service credit under section 403 (b) (13) or section 457 (e) (17) in accordance with paragraph 4 of Regulations section 1.403 (b)-10 (b) and Regulations section 1.457-10 (b) (8). However, you must report:

Can you convert a traditional IRA to a Roth IRA?

A conversion of a traditional IRA to a Roth IRA, and a rollover from any other eligible retirement plan to a Roth IRA, made in the participant’s tax years beginning after December 31, 2017, cannot be recharacterized as having been made to a traditional IRA.

What is a 1099-R?

File Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., for each person to whom you have made a designated distribution or are treated as having made a distribution of $10 or more from profit-sharing or retirement plans, any individual retirement arrangements (IRAs), annuities, pensions, insurance contracts, survivor income benefit plans, permanent and total disability

Who must file 1099-R?

The payer, trustee, or plan administrator must file Form 1099-R using the same name and employer identification number (EIN) used to deposit any tax withheld and to file Form 945, Annual Return of Withheld FederalIncome Tax.

How long to give a rollover notice?

The explanation must be provided no more than 180 days and no fewer than 30 days before making an eligible rollover distribution or before the annuity starting date. However, if the recipient who has received the section 402(f) notice affirmatively elects a distribution, you will not fail to satisfy the timing requirements merely because you make the distribution fewer than 30 days after you provided the notice as long as you meet the requirements of Regulations section 1.402(f)-1, Q/A-2. The electronic section 402(f) notice must meet the requirements for using electronic media in Regulations section 1.401(a)-21.The notice must explain the rollover rules, the special tax treatment for certain lump-sum distributions, the direct rollover option (and any default procedures), the mandatory 20% withholding rules, and an explanation of how distributions from the plan to which the rollover is made may have different restrictions and tax consequences than the plan from which the rollover is made.

Is Section 415 a rollover?

Distributions to correct a section 415 failure are not eligible rollover distributions although they are subject to federal income tax withholding under section 3405. They are not subject to social security, Medicare, or Federal Unemployment Tax Act (FUTA) taxes. In addition, such distributions are not subject to the 10% early distribution tax under section 72(t).

What is an X in a tax return?

Enter an “X” in this box only if the payment shown in box 1 is a total distribution. A total distribution is one or more distributions within 1 tax year in which the entire balance of the account is distributed. If periodic or installment payments are made, mark this box in the year the final payment is made.

What is a direct rollover?

A direct rollover is the direct payment of the distribution from a qualified plan, a section 403(b) plan, or

Self-employed health insurance deduction for Medicare premiums

Self-employed people (who earn a profit from their self-employment) are allowed to deduct their health insurance premiums on Schedule 1 of the 1040, as an “above the line” deduction — which means it lowers their AGI.

Above-the-line deduction for people who are self-employed

If you’re self-employed, the self-employed health insurance deduction — putting your Medicare premiums on Schedule 1 of your 1040 — is the most direct way to reduce your tax burden. And as noted above, this is an “above-the-line” deduction, which means it reduces your adjusted gross income.

Additional considerations

So, let’s review: You’re self-employed, your business made money (congratulations!), and you’re ready to file. Here are few more things to remember before you get started.

Another alternative: Using your HSA funds to pay Medicare premiums

If you have a health savings account (HSA) , know that you can withdraw tax-free money from the account and use it to pay your premiums for Medicare Parts A, B, C, and D (but not Medigap premiums). This is an alternative to deducting your premiums on your tax return, since you can’t do both.