If you (or your spouse, if filing jointly) received Archer MSA or Medicare Advantage MSA distributions in 2021, you must file Form 8853 with Form 1040, 1040-SR, or 1040-NR even if you have no taxable income or any other reason for filing Form 1040, 1040-SR, or 1040-NR. Specific Instructions Name and social security number (SSN).

Do you have to pay taxes on Medicare Advantage contributions?

Contributions can be made only by Medicare. The contributions aren’t included in your income. Distributions from a Medicare Advantage MSA that are used to pay qualified medical expenses aren’t taxed. A health FSA may receive contributions from an eligible individual. Employers may also contribute.

What information does a provider have to report to the IRS?

The information that a provider must report to the IRS includes the following: The name, address, and employer identification number (EIN) of the provider; The responsible individual’s name, address, and TIN, or date of birth if a TIN is not available.

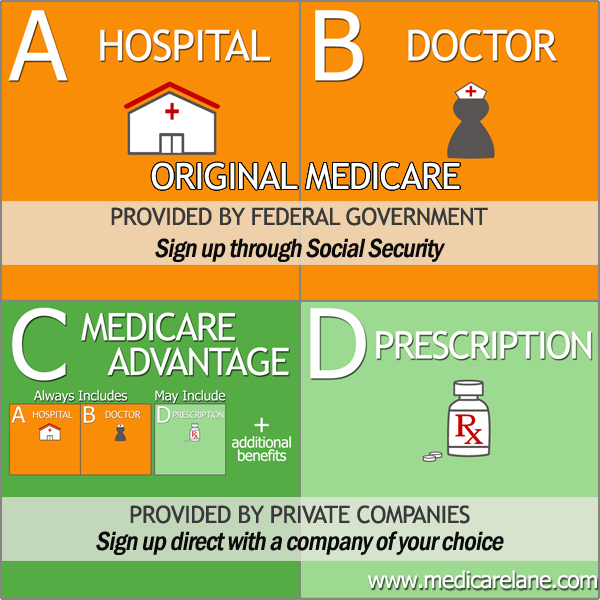

Are Medicare Advantage MSA contributions taxable to the account holder?

To be eligible for a Medicare Advantage MSA, you must be enrolled in Medicare and have an HDHP that meets the Medicare guidelines. Contributions to the account can be made only by Medicare. The contributions and any earnings, while in the account, aren't taxable to the account holder.

Can I contribute to a Medicare Retirement Account?

Contributions to the account can be made only by Medicare. The contributions and any earnings, while in the account, aren't taxable to the account holder. A distribution used exclusively to pay for the qualified medical expenses of the account holder isn't taxable.

Do I have to report 1095-B on my tax return?

You do not need 1095-B form to file taxes. It is for your records. IRS 1095-B form is your proof of the month(s) during the prior year that you received qualifying health coverage.

Do you get a 1095 for Medicare?

If you were enrolled in Medicare: For the entire year, your insurance provider will not send a 1095 form. Retirees that are age 65 and older, and who are on Medicare, may receive instructions from Medicare about how to report their health insurance coverage.

What happens if I don't file my 1095-B?

Good news the 1095-B does not need to be filed! You don't need your form 1095-B to file your tax return. TurboTax will ask you questions about your health coverage but your form 1095-B isn't needed. Just keep the form for your files.

Do I need a 1095-C to file my taxes?

Although information from the Form 1095-C – information about an offer of employer provided coverage - can assist you in determining eligibility for the premium tax credit, it is not necessary to have Form 1095-C to file your return.

How do I get my 1099 from Medicare?

Call 1-800-MEDICARE (1-800-633-4227). TTY users can call 1-877-486-2048. People can reference CMS Product No. 11865 when calling Medicare with questions about this notice.

Do you report Medicare on taxes?

Your Medicare premiums, however, won't be taken out pretax. You'll need to deduct them when you file your taxes instead. This is the case even if you pay your premiums by having the money deducted from your Social Security retirement benefits check.

What is the difference between Form 1095-B and 1095-C?

The 1094-C is the transmittal form that must be filed with the Form 1095-C. Form 1095-B is used to report certain information to the IRS and to taxpayers about individuals who are covered by minimum essential coverage and therefore are not liable for the individual shared responsibility payment.

Do I need a 1095-B to file my taxes 2021?

You no longer have to file the information from your Form 1095-B on your tax return as the federal mandate for having health insurance ended with 2019 returns. Again, you do not have to file Form 1095-B on your 2021 Tax Return. If you have received a 1095-B from your employer, you can just keep a copy for your records.

Why did I get a 1095-B and not a 1095-A?

You need a 1095-A only if you bought health insurance through the Marketplace in 2021. If you did not buy that insurance, then you won't get a 1095-A.

How do I submit my 1095-C to the IRS?

Forms 1095-C are filed accompanied by the transmittal form, Form 1094-C. An ALE Member can provide the required statement to the employer's full-time employees by furnishing a copy of the Form 1095-C filed with the IRS. Alternatively, these returns and employee statements may be provided by using substitute forms.

What is the penalty for not filing 1095-C?

Keep in mind, there is a penalty on furnishing and filing. So, the $280 penalty is doubled to $560 per return if they were not filed or furnished. This can add up quickly as a 1095-C is necessary for every full-time employee.

Do you still need a 1095-C for 2021 taxes?

Taxpayers do not need to wait to receive Form 1095-C before filing their 2021 tax returns; however, you should keep this document with your tax records. Think of the form as your “proof of insurance” for the IRS.

Who is responsible for reporting health insurance coverage?

The health insurance issuer or carrier is responsible for reporting that health coverage. However, if the employer is subject to the employer shared responsibility provisions in section 4980H, it is responsible for reporting information under section 6056 about the coverage it offers to its full-time employees.

Who is not a provider of health coverage under section 6055?

An employer that sponsors an insured health plan (a health plan that provides coverage by purchasing insurance from a health insurance issuer) will not report as a provider of health coverage under section 6055. The health insurance issuer or carrier is responsible for reporting that health coverage.

What is a health insurance issuer?

Health insurance issuers, or carriers, for insured coverage (but see below regarding certain limited exceptions), Plan sponsors of self-insured group health plan coverage, and. The executive department or agency of a governmental unit that provides coverage under a government-sponsored program. 5.

When do you have to furnish a health insurance statement?

A health coverage provider generally must furnish the statement to the responsible individual on or before January 31 of the year following the calendar year in which minimum essential coverage is provided. If the provider applies to the IRS in writing and shows good cause, the IRS may grant an extension of time up to 30 days for the provider to furnish the statement.

Who may report under section 6055?

Plan sponsors in a controlled group that is not an applicable large employer member (ALE Member) under section 4980H, and coverage providers (such as issuers) that are not reporting as employers, may report under section 6055 as separate entities, or may have one entity report for the controlled group. See our section 6056 questions and answers and Forms 1094-C and 1095-C questions and answers for additional information on reporting by ALE Members that are providers of self-insured group health plan coverage.

Can a health care provider report a health care provider?

Yes. Reporting arrangements between health care providers and other parties are not prohibited. However, entering into a reporting arrangement does not transfer the potential liability of the provider for failure to report information and furnish statements under section 6055. In addition, if a person who prepares returns or statements under section 6055 is a tax return preparer, that person will be subject to the requirements generally applicable to tax return preparers.

Do you report catastrophic health insurance?

No. An issuer should not report on coverage under a qualified health plan in the individual market enrolled in through a Marketplace. The Marketplaces will separately report information on enrollments in a qualified health plan to the IRS and individuals under section 36B (f) (3). Under Notice 2017-41 PDF, issuers of catastrophic plan coverage may, but are not required to, report on catastrophic plan coverage enrolled in through the Marketplace for 2015, 2016, and 2017. The Treasury Department and the IRS encourage issuers to voluntarily report on catastrophic plan coverage enrolled in though the Marketplace.

What are qualified medical expenses for Archer MSA?

Generally, qualified medical expenses for Archer MSA purposes are unreimbursed medical expenses that could otherwise be deducted on Schedule A (Form 1040). See the Instructions for Schedule A (Form 1040), Itemized Deductions, and Pub. 502, Medical and Dental Expenses. Qualified medical expenses are those incurred by the account holder or the account holder's spouse or dependent (s). Amounts paid for menstrual care products shall be treated as paid for medical care. See the instructions for Line 7, later. You can't treat insurance premiums as qualified medical expenses unless the premiums are for:

How to figure out your excess contributions?

To figure your excess contributions, subtract your deductible contributions (line 5) from your actual contributions (line 2). However, you can withdraw some or all of your excess contributions for 2020 and they will be treated as if they hadn't been contributed if:

What form do I file for Archer MSA?

If you (or your spouse, if filing jointly) received Archer MSA or Medicare Advantage MSA distributions in 2020, you must file Form 8853 with Form 1040, 1040-SR, or 1040-NR even if you have no taxable income or any other reason for filing Form 1040, 1040-SR, or 1040-NR. .

How much is married filing separately?

Married filing separately. If you have an HDHP with family coverage and are married filing separately, enter only 37.5% (0.375) (one-half of 75%) of the annual deductible for each month on the worksheet; or, if you and your spouse agree to divide the 75% of the annual deductible in a different manner, enter your share.

How long can you withdraw from a tax return?

If you timely filed your return without withdrawing the excess contributions, you can still make the withdrawal no later than 6 months after the due date of your tax return, excluding extensions. If you do, file an amended return with "Filed pursuant to section 301.9100-2" written at the top. Include an explanation of the withdrawal. Make all necessary changes on the amended return (for example, if you reported the contributions as excess contributions on your original return, include an amended Form 5329 reflecting that the withdrawn contributions are no longer treated as having been contributed).

When to include contributions to Archer MSA?

Include on line 2 contributions you made to your Archer MSA in 2020. Also include those contributions made from January 1, 2021, through April 15, 2021, that were for 2020. Don't include amounts rolled over from another Archer MSA. See Rollovers, later.

Who must file Form 8853?

Who Must File. You must file Form 8853 if any of the following applies. You (or your employer) made contributions for 2020 to your Archer MSA. You are filing a joint return and your spouse (or his or her employer) made contributions for 2020 to your spouse's Archer MSA.

Why is Medicare going broke?

Medicare is in a financial crisis and risks going broke. One reason is because 10% of Medicare payments are lost to fraud, including those cheating or defrauding Medicare Advantage plans.

Can you report Medicare Advantage fraud?

If you properly report Medicare Advantage or Part C fraud, you may be entitled to a significant whistleblower reward. If you want former Justice Department Attorney Joel Hesch to evaluate in complete confidence to see if you have the right type of case to get a reward, then fill out the form at this link (click here) and Mr. Hesch will personally get back to you right away.

How to order IRS forms?

Ordering tax forms, instructions, and publications. Go to IRS.gov/OrderForms to order current forms, instructions, and publications; call 800-829-3676 to order prior-year forms and instructions. The IRS will process your order for forms and publications as soon as possible.

How much is the deductible for a family plan?

The annual deductible for the family plan is $3,500. This plan also has an individual deductible of $1,500 for each family member. The plan doesn’t qualify as an HDHP because the deductible for an individual family member is less than the minimum annual deductible ($2,800) for family coverage.

When is HSA deductible for telehealth?

HSA. Telehealth and other remote care coverage with plan years beginning before 2022 is disregarded for determining who is an eligible individual. A high deductible health plan (HDHP) year beginning before 2022 may have a $0 deductible for telehealth and other remote care services.

Do you have to meet the deductible for one family member?

Under these plans, if you meet the individual deductible for one family member, you don’t have to meet the higher annual deductible amount for the family.

Is over the counter medicine considered medical care?

Over-the-counter medicine (whether or not prescribed) and menstrual care products are treated as medical care for amounts incurred after 2019. HRA. Over-the-counter medicine (whether or not prescribed) and menstrual care products are treated as medical care for amount s incurred after 2019.

Can an HSA be deducted from an employer?

An HSA may receive contributions from an eligible individual or any other person, including an employer or a family member, on behalf of an eligible individual. Contribution s, other than employer contributions , are deductible on the eligible individual’s return whether or not the individual itemizes deductions.