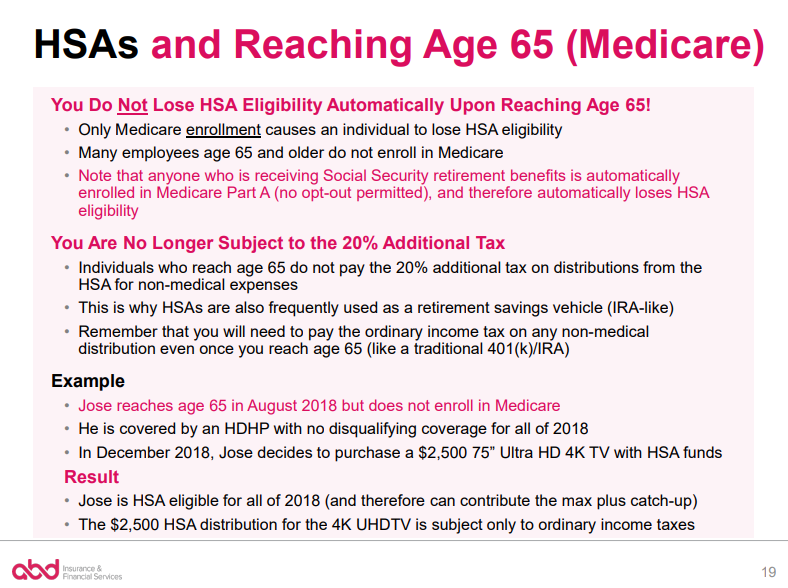

- Once you enroll in Medicare, you’re no longer eligible to contribute funds to an HSA.

- However, you can use existing money in an HSA to pay for some Medicare costs.

- You’ll receive a tax penalty on any money you contribute to an HSA once you enroll in Medicare.

How do you start a HSA account?

You can set up your account with:

- Banks

- Brokers and financial advisors

- Credit Unions

- Insurance Companies

What is the penalty for having a HSA and Medicare?

Understanding the HSA Withdrawal Penalty and Other Useful Information

- HSA Basics. In some ways, an HSA is similar to a Flexible Spending Account (FSA). ...

- Non-qualified expenses and the HSA withdrawal penalty. One significant perk of an HSA is that once you reach age 65, you can withdraw funds for any expense without penalty.

- Mistake Forgiveness. The IRS does allow some leeway for honest mistakes. ...

- HSA Facts You Should Know. ...

Can I enroll in Medicare if I have a HSA?

Can I enroll in Medicare if I have a health savings account? A. Once you sign up for Medicare, you’re no longer eligible to contribute to a health savings account (HSA), so in some cases, it pays to hold off on enrolling. Health savings accounts offer a great opportunity to sock away funds on a tax-free basis to pay for healthcare costs ...

Can I pay for health insurance using my HSA account?

Your health savings account (HSA) may be used to pay for many IRS-approved medical expenses, including qualified health insurance premiums. Premiums paid for COBRA insurance, Medicare, and long-term care insurance may be HSA-eligible. All qualified health insurance premiums that are covered by an HSA are 100% tax-free.

What happens to HSA money when you go on Medicare?

Although you can't make any more contributions to your HSA once you're enrolled in Medicare, your HSA will continue to provide tax-free funds to cover medical costs until you use up all the money in your account. You also have the option to use your HSA funds as a regular retirement account after you turn 65.

When should I stop HSA contributions before Medicare?

If you have to (or choose to) enroll in Medicare Part A, the coverage is retroactive for up to 6 months, but no earlier than your eligibility date. Because of this, you should plan to stop HSA contributions around 6 months before enrolling in Medicare.

What happens to my HSA when I turn 65?

At age 65, you can take penalty-free distributions from the HSA for any reason. However, in order to be both tax-free and penalty-free the distribution must be for a qualified medical expense. Withdrawals made for other purposes will be subject to ordinary income taxes.

Why do I have to stop contributing to my HSA 6 months before Medicare?

This is because when you enroll in Medicare Part A, you receive up to six months of retroactive coverage, not going back farther than your initial month of eligibility. If you do not stop HSA contributions at least six months before Medicare enrollment, you may incur a tax penalty.

Can my spouse use my HSA if they are on Medicare?

Yes, being eligible to contribute to the HSA is determined by the status of the HSA account holder not the dependents of the account holder. Your spouse being on Medicare does not disqualify you from continuing contributions to the HSA up to the family limit, even if they are also covered by the HDHP.

Do you have to pay taxes on HSA after 65?

At age 65, you can withdraw your HSA funds for non-qualified expenses at any time although they are subject to regular income tax. You can avoid paying taxes by continuing to use the funds for qualified medical expenses.

Can I keep my HSA after retirement?

Once you turn 65, you can still contribute to your HSA post-retirement as long as you aren't enrolled in Medicare and have a qualifying HDHP. The simple answer is: Yes!

What is the tax rate for Medicare after a HSA?

Excess contributions will be taxed an additional 6 percent when you withdraw them. You’ll pay back taxes plus an additional 10 percent tax if you enroll in Medicare during your HSA testing period.

What is an HSA account?

A health savings account (HSA) is an account you can use to pay for your medical expenses with pretax money. You can put money in an HSA if you meet certain requirements. You must be eligible for a high-deductible health plan and you can’t have any other health plan. Because Medicare is considered another health plan, ...

How long do you have to be on Medicare before you turn 65?

When you enroll in Medicare after you turn age 65, the IRS will consider you to have had access to Medicare for 6 months prior to your enrollment date. In general, it’s a good idea to stop HSA contributions if you’re planning to enroll in Medicare anytime soon. That way, you can avoid any tax penalties and save money.

What is Medicare Part B?

Medicare Part B (medical insurance) has standard costs, including a monthly premium and an annual deductible. Additionally, you’ll pay 20 percent of the Medicare-approved cost for most covered services. You can use the funds in your HSA toward any of these costs.

Does MSA money count toward deductible?

So while you can spend your MSA funds on a service Medicare doesn’t cover, it won’t count toward your deductible.

Is MSA the same as HSA?

This plan is similar to an HSA, but there are a few key differences. Just like a standard HSA, you’ll need to be enrolled in a high-deductible plan. With an MSA, this means you’ll need to select a high-deductible Medicare Advantage plan. Once you’ve selected a plan, things will look a little different than your HSA.

Can a 65 year old retire without Medicare?

As another example, let’s say a retired person chooses not to enroll in Medicare when they turn 65 years old. They don’t have another health plan and pay all health costs out of pocket. In this case, they’ll pay a late enrollment penalty if they do decide to enroll in Medicare later.

Is HSA taxed?

Funds contributed to an HSA are not taxed when put into the HSA or when taken out, as long as they are used to pay for qualified medical expenses. Your employer may oversee your HSA, or you may have an individual HSA that is overseen by a bank, credit union, or insurance company.

Can you use HSA for qualified medical expenses?

If you use the account for qualified medical expenses, its funds will continue to be tax-free. Whether you should delay enrollment in Medicare so you can continue contributing to your HSA depends on your circumstances.

Does HDHP have a deductible?

HDHPs have large deductibles that members must meet before receiving coverage. This means HDHP members pay in full for most health care services until they reach their deductible for the year. Afterwards, the HDHP covers all the member’s costs for the remainder of the year.

What is an HSA?

An HSA stands for a health savings account. People who have HDHPs will often utilize HSAs as a way to save money on healthcare expenses. HDHPs are those that usually cover preventive health services and have a high deductible of at least $1,400 for an individual or $2,800 for a family, according to Healthcare.gov.

What happens if you don't meet your HSA deductible?

If a person finds they do not meet their high deductible for the year, yet contributed the maximum amount to their HSA, the money can roll over and keep earning interest. When a person retires, and they have money in their HSA, they can use this money to help pay for Medicare expenses.

Why do people contribute to HSA?

Some people will contribute a significant amount to their HSA in preparation for their retirement. When they retire and start to receive Medicare benefits , they can then use the HSA to pay for health expenses.

What is the Medicare Part B copayment?

For Medicare Part B, this comes to 20%. Copayment: This is a fixed dollar amount that an insured person pays when receiving certain treatments. For Medicare, this usually applies to prescription drugs.

What is the difference between coinsurance and deductible?

Coinsurance: This is a percentage of a treatment cost that a person will need to self-fund. For Medicare Part B, this comes to 20%.

What happens if you don't use your HSA?

If a person does not use their HSA in a year, the funds can roll over into the next year. The HSA can earn interest, and the government will not tax a person on interest earned. Also, as long as a person uses the funds to pay for qualifying healthcare expenses, they will not pay tax on removing the funds.

Do HDHPs count towards income?

An employer can also contribute to an HSA, and the contribution does not count toward a person’s income, meaning they will not be taxed.

How long do you have to stop HSA before enrolling in Medicare?

There is a six - month lookback period (but not before the month of reaching age 65) when enrolling in Medicare after age 65, so a best practice is for workers to stop contributing to their HSA six months before enrolling in Medicare to avoid penalties. See the examples below for more on this.

When did HSA start?

Image by Roy Scott/IKON Images. Before the tax - savings wonder that is the health savings account (HSA) was introduced in 2003, it was a generally accepted best practice for any worker who wasn't already collecting Social Security at the age of 65 to go ahead and sign up for Medicare Part A (hospital insurance), regardless of other coverage.

What happens if you miss the deadline for Medicare?

In other words, getting the Medicare Special Enrollment Period wrong risks a gap in coverage plus a lifetime of penalties.

Can HSA funds be used for medical expenses?

See the examples below for more on this. Funds already in the HSA can still be used for qualified medical expenses upon enrollment in Medicare, including to reimburse taxpayers for Medicare premiums (but not premiums for Medicare supplemental insurance) as well as to pay for long - term - care costs and insurance.

How to open an HSA?

According to federal guidelines, you can open and contribute to a HSA if you : 1 Are covered under a qualifying high-deductible health plan which meets the minimum deductible and the maximum out of pocket threshold for the year 2 Are not covered by any other medical plan, such as that for a spouse 3 Are not enrolled in Medicare 4 Are not enrolled in TRICARE or TRICARE for Life 5 Are not claimed as a dependent on someone else's tax return 6 Are not covered by medical benefits from the Veterans Administration 7 Do not have any disqualifying alternative medical savings accounts, like a Flexible Spending Account or Health Reimbursement Account

How much can I save with an HSA?

High income earners choosing a HDHP can potentially use HSAs to save up to $8,100 per year in a tax-sheltered account. For both high income earners and those approaching retirement, the HSA can be a worthwhile vehicle for building a medical emergency fund while also saving in a type of alternative retirement vehicle .

What is HDHP insurance?

Generally speaking, a HDHP is a healthcare plan that trades relatively low premiums for relatively high deductibles, as its name implies. To qualify for a HSA that can be opened in combination with a HDHP, the HDHP must meet certain criteria.

Why are HSAs important?

HSAs as Savings/Investing Tools. HSAs offer a tax shelter. For savvy investors this can create an opportunity to accumulate capital gains that can be withdrawn tax-free for medical expenses. Investment options, of course, can become more important if you have a larger HSA balance.

What can I use my HSA for?

The funds in your HSA can be used to pay for qualified medical expenses incurred by you, your spouse, and your dependents. The IRS establishes what is and what is not a qualified medical expense, detailed in IRS Publication 502, Medical and Dental Expenses.

How much can I contribute to my HSA in 2020?

For 2020, the maximum contribution amounts are $3,550 for individual coverage and $7,100 for family coverage.

When was HSA established?

HSAs were established in 2003, as part of the Medicare Prescription Drug, Improvement, and Modernization Act.

What happens to my HSA once I enroll in medicare?

When you enroll in Medicare, you can continue to withdraw money from your HSA. The money is yours forever. Your HSA dollars can cover qualified medical expenses — 100% tax-free — if your insurance doesn’t reimburse you.

Are there penalties for having both an HSA and Medicare?

The IRS won’t penalize you if you still have money in your HSA when you enroll in Medicare. You can use your HSA dollars to pay for qualified medical expenses if you want to save money on taxes. Unlike a flexible spending account (FSA), all the unused funds in your HSA will continue to roll over every year.

What costs are not covered by Medicare?

Before you apply for Medicare, you should review your major out-of-pocket costs. This will help you determine the best time to apply for coverage.

What happens when I buy an eligible expense vs. an ineligible expense with HSA funds?

When you turn 65, you will have more flexibility over how you use the funds in your HSA. You can pay for all qualified expenses, free of taxes. You’ll have to pay income tax on money you withdraw to pay for nonqualified expenses. If you’re under 65, you may also owe a 20% tax penalty.

Are my withdrawals for HSA tax-free?

One of the benefits of an HSA is that your withdrawals can be tax-free if used for qualified medical expenses. All nonqualified expenses will be subject to federal and state income taxes.

The bottom line

Enrolling in Medicare can affect your ability to make contributions to a health savings account (HSA). Before you sign up for Medicare, make sure you understand HSA rules to avoid unexpected taxes and penalties. Although Medicare beneficiaries cannot contribute to an HSA, they can still withdraw money from the account.

What is an HSA account?

A Health Savings Account (HSA) is a tax-exempt trust or custodial account you set up with a qualified HSA trustee to pay or reimburse certain medical expenses you incur. You must be an eligible individual to qualify for an HSA.

When is HSA deductible for telehealth?

HSA. Telehealth and other remote care coverage with plan years beginning before 2022 is disregarded for determining who is an eligible individual. A high deductible health plan (HDHP) year beginning before 2022 may have a $0 deductible for telehealth and other remote care services.

What is the maximum HSA contribution for 2020?

. If you had family HDHP coverage on the first day of the last month of your tax year, your contribution limit for 2020 is $7,100 even if you changed coverage during the year. .

How long does it take to rollover an Archer MSA?

Generally, any distribution from an Archer MSA that you roll over into another Archer MSA or an HSA isn’t taxable if you complete the rollover within 60 days. An Archer MSA and an HSA can receive only one rollover contribution during a 1-year period. See the Form 8853 instructions for more information.

What is HDHP in health insurance?

High deductible health plan (HDHP). An HDHP has: A higher annual deductible than typical health plans, and. A maximum limit on the sum of the annual deductible and out-of-pocket medical expenses that you must pay for covered expenses.

How much is the deductible for a family plan?

The annual deductible for the family plan is $3,500. This plan also has an individual deductible of $1,500 for each family member. The plan doesn’t qualify as an HDHP because the deductible for an individual family member is less than the minimum annual deductible ($2,800) for family coverage.

When is the last month of HDHP coverage?

Under the last-month rule, if you are an eligible individual on the first day of the last month of your tax year (December 1 for most taxpayers), you are considered an eligible individual for the entire year. You are treated as having the same HDHP coverage for the entire year as you had on the first day of the last month if you didn’t otherwise have coverage.